You might have heard about the CSRD (Corporate Sustainability Reporting Directive) already since it was adopted back in 2022. But now, with the first year of adoption upon us, are you aware how it’s impacting UK companies with EU operations?

In this guide, we’ve pulled together all the key information, including what should be on your radar and the answers to some of the most common CSRD questions.

What is CSRD? What is ESRS? And how are they linked?

CSRD sets out the high-level sustainability information that companies in scope need to report on. These CSRD reports, however, need to be prepared using the European Sustainability Reporting Standards (ESRSs).

ESRSs set out detailed reporting requirements for CSRD reporters over 12 standards. The standards are topical and include but aren’t limited to areas such as climate change, pollution, resource use and circular economy, biodiversity, workers, business conduct, etc.

Which topics each company reports under will be determined by a mandatory double materiality assessment. This assessment considers not only the company’s operations but also its entire value chain, both downstream and upstream. It looks at a company’s financial risks and opportunities as a result of ESG topics (an outside-in view), as well as the impact the company has on people and the environment (an inside-out view).

The requirements will become effective in stages, based on the characteristics of reporters, with earliest application from 1 January 2024 to 1 January 2028.

What does this mean for UK companies?

The Corporate Sustainability Reporting Directive (CSRD) will directly affect UK companies if:

- They have securities listed on EU regulated markets; or

- If they generate more than €150m net turnover in the EU (for each of the last two consecutive financial years) and have at least one EU subsidiary (large or listed on an EU regulated market) or EU branch (more than €50m net turnover in the preceding financial year).

It will also apply directly to EU subsidiaries of UK companies. This may be as soon as periods commencing on or after 1 January 2024 for UK companies with securities listed on an EU regulated market with more than 500 employees.

CSRD Timeline

CSRD will be implemented over a 4-stage approach:

Are there any exemptions?

A subsidiary (except large-listed subsidiary) is exempt from preparing a CSRD report when:

- It is included in the consolidated management report of a parent undertaking prepared in accordance with the EU Accounting Directive; and

- The assurance opinion on the consolidated sustainability reporting is publicly available.

Subsidiaries (including EU subsidiaries) of a non-EU parent may also take this exemption if the parent reports under CSRD or standards that are deemed to be equivalent by the EU.

However, the exemption is only available if the parent undertaking’s reporting at the consolidated level provides an adequate understanding of the risks and impacts of its subsidiaries and information on the due diligence processes where there are differences with those of the group.

An exempted subsidiary must disclose certain information about the fact the exemption has been taken too.

Where should the disclosures be made?

The CSRD requires the ESRS disclosures in a dedicated section within the management report. This is important to note, as it differs from other reporting frameworks, such as TCFD, which allows companies to make disclosures outside of the annual report.

Companies must digitally tag reported sustainability information in accordance with a digital taxonomy, which will help users quickly locate the information they need.

Is assurance mandatory?

The short answer: YES. From the first year of CSRD application, companies are required to obtain limited assurance over their compliance with the ESRS standards, their underlying double materiality assessment process, and certain reported indicators. The level of assurance has been indicated by the EU to move towards reasonable assurance if assessed as feasible in the future.

The assurance report must be provided by a statutory or financial auditor and be publicly disclosed in the annual financial report.

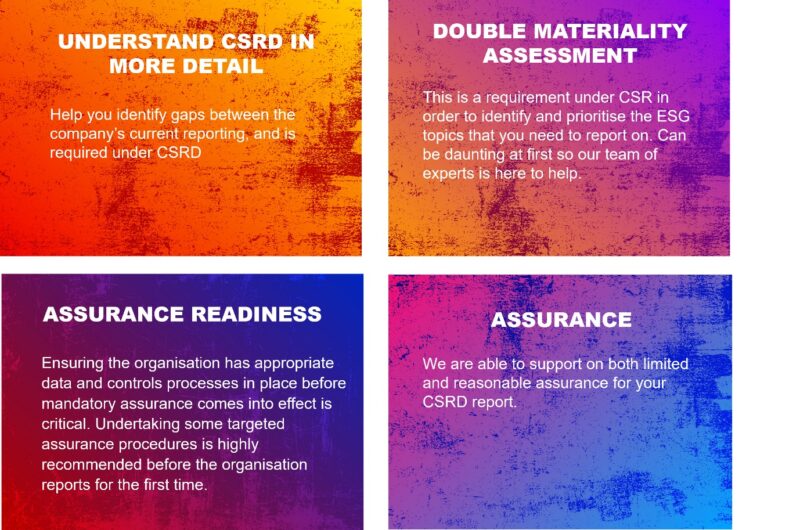

Questions? Cooper Parry can help

CSRD is a significant and complex change in ESG reporting. Early preparation is critical to ensure a smooth implementation that can be subject to an external assurance engagement.

Our Sustainability team can support you as you embark on this journey. Here’s a flavour of how we can help: