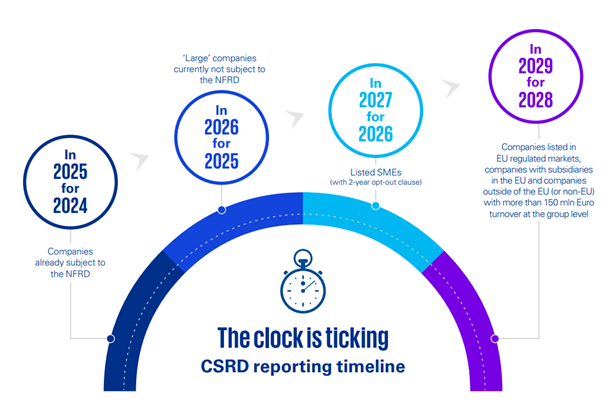

The EU’s Corporate Sustainability Reporting Directive (CSRD) is transforming ESG reporting. Starting from 2024, almost 50,000 companies are subject to mandatory sustainability reporting, including non-EU companies which have subsidiaries operating within the EU or are listed on EU regulated markets. The latter will come into effect in 2029 for financial year 2028.

So what? UK companies with a turnover of more than EUR150 million in the EU, with at least one subsidiary or a branch in the EU territory with turnover of more than EUR40 million in the EU, must publish a sustainability report from 2028 on. The sustainability report requirements are exhaustive, so affected companies need to establish processes as early as possible.

The first CSRD reports are due in 2025 – for companies with year ending 31 December 2024. The key changes under the CSRD are as follows:

- Many more companies will have to report on sustainability information, including small and medium-sized businesses and organisations headquartered outside the EU.

- The sustainability report must be disclosed as part of the management report.

- The principles of double materiality (impact and financial materiality) applies.

- Disclosure requirements topics include biodiversity, resource use, treatment of your own and suppliers’ workforce, and business conduct.

- Full integration of the EU taxonomy.

- Limited assurance of sustainability reporting is mandatory.

Many companies within the EU and beyond must report in compliance with the CSRD. This includes all companies listed on the EU regulated markets, although small and medium-sized enterprises (SMEs) will not have to comply until January 2026 and even have an “opt-out” clause until 2028.

Added to this are companies of a certain size, referred to as “large undertakings”, which may be EU companies or EU subsidiaries of companies from outside of the EU. These companies must fulfil two out of the following three criteria:

- net turnover of EUR40 million.

- a balance sheet of EUR20 million.

- a minimum of 250 employees.